How startup equipment financing works: Options and steps

You’ve probably heard that only established businesses can secure equipment financing. That’s a myth. In reality, over 80% of businesses use financing or leasing to acquire the tools they need, and startups are no exception. Whether you’re launching a manufacturing operation, opening a restaurant, or building a tech company, equipment financing offers a practical path to acquiring essential assets without draining your cash reserves. This guide walks you through the real-world options, approval processes, and strategic decisions that will help you secure the equipment your startup needs to grow.

Table of Contents

- What is equipment financing for startups?

- How equipment financing works: Process and requirements

- Types of equipment financing: Loans vs. leases

- Who provides equipment financing? Startup lender options

- What to watch for: Edge cases, pitfalls, and expert advice

- Making the right choice for your startup: Practical steps

- Take your next step: From equipment to growth

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Startup access possible | Most startups can obtain equipment financing even with limited history, though terms may be stricter. |

| Loans vs. leases differ | Loans offer ownership and equity while leases give flexibility and lower initial payments. |

| Personal credit matters | Your personal credit score is a critical factor for approval in early-stage financing. |

| Many lender options | Banks, SBA programs, and online lenders all provide equipment funding to new businesses. |

| Choose based on needs | Match your financing method to the type and life of the equipment for best results. |

What is equipment financing for startups?

Now that we’ve set the stage for why this topic matters, let’s break down what equipment financing actually means for startups.

Equipment financing for startups allows acquisition of machinery, vehicles, and technology without paying the full cost upfront. The equipment itself serves as collateral, which means lenders have security even when your business is brand new. This structure preserves your working capital for payroll, marketing, and other operational needs that can’t be financed.

Here’s how it typically works: the lender pays the vendor directly, and you repay the loan over two to seven years through fixed monthly payments that include both principal and interest. Because the equipment backs the loan, approval requirements are often more flexible than traditional business loans. This makes equipment financing particularly valuable for founders who need to build operational capacity quickly.

“Equipment financing transforms capital expenditures into manageable monthly costs, allowing startups to deploy resources where they matter most: growth and customer acquisition.”

The types of equipment you can finance include:

- Manufacturing machinery and production equipment

- Commercial vehicles and transportation assets

- Restaurant and food service equipment

- Medical and dental devices

- Technology infrastructure and servers

- Construction and heavy equipment

For startups exploring multiple funding pathways, equipment financing offers a focused solution that doesn’t dilute ownership or require giving up equity. It’s a tool that lets you build the infrastructure your business needs while maintaining control and flexibility.

How equipment financing works: Process and requirements

With the basics defined, let’s walk through the practical steps and what you’ll need to qualify.

The equipment financing process follows a clear sequence that most startups can navigate in two to four weeks:

- Identify your equipment needs and gather vendor quotes with detailed specifications

- Research lenders who specialize in your industry or equipment type

- Submit your application with financial documents, business plan, and equipment details

- Undergo credit review where lenders assess both business and personal creditworthiness

- Receive approval and terms including rate, payment schedule, and down payment requirement

- Close the deal with signed agreements and any required down payment

- Receive equipment as the lender pays the vendor directly

Lenders assess personal credit (often requiring a minimum score of 580 to 680), down payment capacity (ranging from 0% to 20%, with 100% financing possible), business revenue or projections, and equipment resale value. For startups without established business credit, founder credit scores carry significant weight in approval decisions.

Personal guarantees are standard practice for startup equipment financing. This means you’re personally liable if the business can’t make payments. While this adds risk, it’s the trade-off that makes financing accessible to new businesses without extensive operating history.

Pro Tip: Before applying, check your personal credit report and address any errors or issues. A difference of 50 points in your credit score can mean thousands of dollars in interest over the life of your loan.

The approval landscape is surprisingly favorable. Market data shows approval rates for equipment financing hover around 79% to 81%, significantly higher than traditional business loans. This reflects the lower risk profile that collateralized equipment provides to lenders.

Interest rates vary widely based on your credit profile, equipment type, and lender. Expect rates between 8% and 30% APR for startups, with the best rates reserved for founders with strong credit and substantial down payments. Terms typically match the useful life of the equipment, so a delivery van might finance over five years while a computer server finances over three.

Many founders combine equipment financing with other startup funding strategies to create a complete capital stack. Equipment loans handle hard assets while other funding sources cover working capital, inventory, and growth initiatives. This strategic approach, often refined through business education programs, maximizes financial efficiency and minimizes dilution.

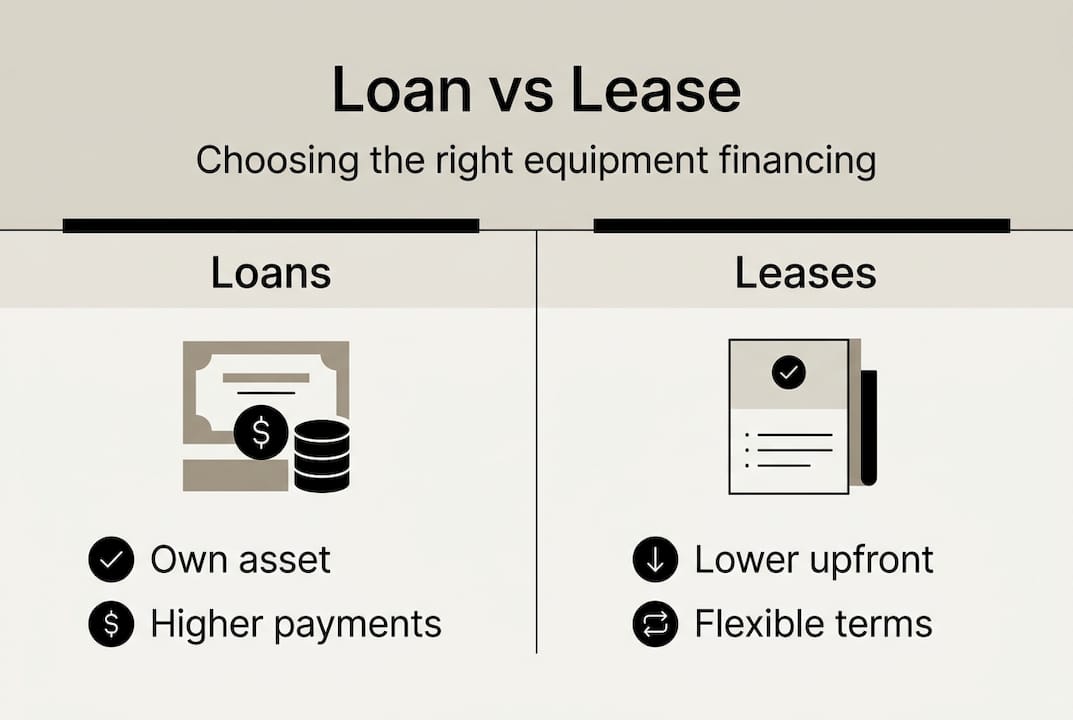

Types of equipment financing: Loans vs. leases

Once you know what the process involves, the next major question is which structure fits your business.

Equipment loans and leases serve different strategic purposes, and choosing the right structure depends on your equipment’s expected lifespan, your cash flow situation, and your long-term business plans.

Equipment loans build equity as you pay down the principal, eventually giving you full ownership of the asset. Payments are typically higher than lease payments, but you can claim depreciation as a tax deduction. Leases, by contrast, provide flexibility with lower monthly payments and the option to upgrade equipment at lease end, though you never own the asset. Lease payments are fully deductible as operating expenses.

| Feature | Equipment Loan | Equipment Lease |

|---|---|---|

| Ownership | You own the asset | Lender owns the asset |

| Monthly payment | Higher | Lower |

| Tax benefit | Depreciation deduction | Full payment deduction |

| End of term | You keep equipment | Return or buy equipment |

| Best for | Long-life assets | Rapidly evolving technology |

| Flexibility | Limited | High |

Loans make sense when you’re financing durable equipment with a long useful life, like manufacturing machinery, commercial ovens, or construction equipment. These assets will serve your business for years, and ownership builds equity on your balance sheet. The higher payments are offset by the long-term value of owning the equipment outright.

Leases shine when you need technology that evolves quickly, like computers, point-of-sale systems, or medical imaging equipment. The lower payments preserve cash flow, and the ability to upgrade at lease end keeps your business competitive without the burden of disposing of obsolete equipment.

Pro Tip: Consider a lease-to-own structure if you want the flexibility of leasing with the eventual benefit of ownership. These hybrid arrangements let you apply a portion of lease payments toward a purchase option at term end.

Your decision should align with your broader business strategy. Founders focused on building asset value and long-term stability often prefer loans. Those prioritizing flexibility and cash flow management lean toward leases. Many successful startups, particularly those that have gone through entrepreneurship education programs, use both structures strategically, financing core equipment while leasing technology that needs regular updates.

For additional perspective on commercial leasing structures, you can explore commercial leasing comparisons that highlight how different industries approach equipment acquisition. The principles of matching financing structure to asset characteristics apply across markets and business types, and understanding these patterns helps you make more informed decisions for your specific situation.

Who provides equipment financing? Startup lender options

Understanding which financial product you need leads to the crucial step: picking the right lender.

Banks, SBA programs, and online lenders each offer equipment financing, but their terms, requirements, and suitability for startups vary significantly.

Traditional banks offer the lowest rates but the strictest requirements. They typically want to see two years of business history, strong revenue, and excellent credit. For most startups, banks are difficult to access unless you have substantial collateral or a strong existing banking relationship.

SBA loan programs provide government-backed financing that reduces lender risk and improves terms for borrowers. SBA 7(a) loans offer up to $5 million with 10% to 20% down payment requirements for startups, while SBA 504 loans can finance up to 90% of fixed asset costs. These programs are specifically designed to support small businesses and startups, making them excellent options if you can navigate the paperwork and wait times.

Online and specialty lenders have emerged as the most accessible option for startups. They use alternative underwriting methods, approve applications quickly (often within 48 hours), and work with newer businesses that traditional lenders reject. The trade-off is higher interest rates, typically ranging from 15% to 30% APR.

| Lender Type | Rate Range | Funding Limit | Approval Speed | Startup Friendly |

|---|---|---|---|---|

| Traditional banks | 6-12% | $50K-$5M+ | 2-6 weeks | Low |

| SBA programs | 7-10% | Up to $5M | 4-8 weeks | Moderate |

| Online lenders | 15-30% | $5K-$500K | 1-3 days | High |

| Equipment vendors | 8-20% | Varies | 1-2 weeks | Moderate |

Equipment vendors and manufacturers often provide financing directly or through captive finance companies. These programs are convenient and sometimes offer promotional rates, but you’re limited to that vendor’s equipment and may miss better deals elsewhere.

The best approach for most startups is to apply with multiple lenders simultaneously. This lets you compare actual offers rather than advertised rates, and it gives you negotiating leverage. Many founders who have completed entrepreneurship bootcamps report that understanding lender motivations and comparison shopping saved them thousands in financing costs.

For startups exploring comprehensive private funding options, equipment financing often works best as part of a broader capital strategy rather than as your sole funding source.

What to watch for: Edge cases, pitfalls, and expert advice

Even with many options, startups face unique challenges and should be alert to these potential pitfalls and trends.

Startups under two years old are often capped at $50,000 in initial financing, even if they need more expensive equipment. Rates can reach 30% APR for founders with limited credit history, and personal guarantees are nearly universal. These constraints mean you need to be strategic about which equipment to finance first and how to build a track record that unlocks better terms later.

Used equipment presents both opportunities and challenges. You can acquire quality assets at lower prices, but lenders scrutinize condition and resale value carefully. Expect more stringent inspections, lower loan-to-value ratios (often 70% to 80% instead of 90% to 100%), and potentially higher rates. The key is working with reputable vendors who can provide equipment history and maintenance records.

Personal guarantees deserve careful consideration. When you sign a personal guarantee, you’re putting your personal assets at risk if the business fails. This is standard practice for startup financing, but you should understand exactly what you’re signing. Some guarantees are limited to the equipment value, while others extend to all business debts.

Pro Tip: Negotiate the scope of your personal guarantee. Some lenders will limit the guarantee to a specific dollar amount or time period, especially if you have strong credit or make a substantial down payment.

Emerging trends are reshaping the equipment financing landscape:

- AI-powered underwriting is accelerating approvals, with some lenders offering same-day decisions

- Green and sustainable equipment incentives are expanding, with lower rates and tax benefits for energy-efficient assets

- Equipment-as-a-Service (EaaS) models are growing, offering pay-per-use arrangements that eliminate traditional financing entirely

- Embedded financing at point of sale is becoming more common, letting you finance equipment directly through vendor platforms

“The future of equipment financing lies in flexibility and speed. Startups no longer need to choose between access and affordability; new models are delivering both.”

These trends create opportunities for savvy founders. If you’re acquiring equipment with environmental benefits, research available incentives before applying for financing. If your equipment needs are variable or seasonal, explore EaaS models that align costs with usage. The equipment financing market is more dynamic and founder-friendly than ever before.

Making the right choice for your startup: Practical steps

With awareness of the landscape and risks, it’s time to plan your own next steps for acquiring equipment.

Financing works best for long-life assets you plan to use for years, while leasing suits short-life technology or situations where rapid upgrades are crucial. Match your financing method to your equipment’s characteristics and your business strategy.

Follow this systematic approach to equipment acquisition:

- Create a detailed equipment list with specifications, costs, and vendors for everything you need

- Prioritize based on impact by identifying which equipment will generate revenue or reduce costs most quickly

- Determine your financing capacity by calculating how much monthly payment your cash flow can support

- Research lender options and gather rate quotes from at least three different sources

- Prepare your application package including business plan, financial projections, and equipment quotes

- Submit applications simultaneously to multiple lenders for comparison

- Negotiate terms using competing offers as leverage for better rates or conditions

- Review agreements carefully before signing, paying special attention to personal guarantee language

When negotiating with vendors or lenders, remember these tactics:

- Ask vendors if they offer financing incentives or can reduce equipment prices for cash purchases

- Request rate reductions by offering a larger down payment or shorter term

- Negotiate prepayment penalties to ensure you can refinance if better terms become available

- Bundle multiple equipment purchases to qualify for volume discounts or better financing terms

First-time applicants should prepare a comprehensive package that tells your business story. Include your business plan, financial projections showing how the equipment will generate returns, personal financial statements, and detailed equipment specifications. The more complete your application, the faster the approval process and the better your terms.

Your equipment financing decision is just one piece of building a sustainable, growing business. The most successful founders approach financing strategically, understanding how each capital decision affects their long-term flexibility and growth potential.

Take your next step: From equipment to growth

Ready to implement your equipment plan? Here’s how Nomad Excel can support your next chapter.

Securing equipment financing solves one critical challenge, but building a thriving startup requires more than just the right tools. You need clarity on your business model, execution frameworks that drive results, and a community of fellow founders who understand the journey you’re on.

Nomad Excel’s online entrepreneurship bootcamp provides the strategic foundation that transforms equipment investments into sustainable growth. Through hands-on learning, expert mentorship, and practical frameworks, you’ll develop the business acumen to make smarter capital decisions and build systems that scale. Our programs connect you with experienced entrepreneurs who have navigated the same financing decisions you’re facing now.

Beyond equipment acquisition, your startup needs a clear growth strategy workflow that aligns your operations, marketing, and financial planning. We help founders build these integrated systems through structured bootcamps that combine education with execution. You’ll leave with not just knowledge, but implemented strategies that drive revenue and efficiency.

Explore how Nomad Excel can accelerate your journey from startup founder to established entrepreneur. Our community of driven founders, proven frameworks, and expert guidance provide the support system that turns equipment investments into lasting business success.

Frequently asked questions

Can I get equipment financing if my business is less than a year old?

Yes, but expect lower funding limits around $50,000, higher interest rates, and requirements for personal guarantees. Lenders rely heavily on your personal credit and down payment capacity when your business lacks operating history.

Is a lease or loan better for startup equipment?

Loans build equity and suit durable assets you want to own long-term, while leases offer flexibility and lower payments for technology that needs frequent updating. Choose based on the equipment’s expected lifespan and your cash flow priorities.

Does my personal credit score affect approval?

Yes, lenders assess personal credit heavily, often requiring minimum scores between 580 and 680 for startup equipment financing. Your personal credit history becomes the primary indicator of creditworthiness when business credit is limited or nonexistent.

Can I finance used or older equipment?

Yes, but used equipment faces scrutiny for condition and resale value before approval. Expect lower loan-to-value ratios and potentially higher rates compared to new equipment financing.

Are there any trends to watch in equipment financing?

AI underwriting is speeding approvals to same-day decisions, green equipment incentives are expanding with better rates, and Equipment-as-a-Service models offer pay-per-use alternatives to traditional financing. These trends create more flexible options for startups.

Recommended

- Guide to private funding for startup business: options

- Crowdfunding for business startup: launch and succeed

- Entrepreneurship Bootcamp Step by Step: Launch and Scale Fast

- What Is Early-Stage Entrepreneurship? Complete Guide

- Commercial Coffee Machine Rental Devon Somerset | Lease Options

Comments are closed.